8 min read · Budgeting · Wealth Building

|

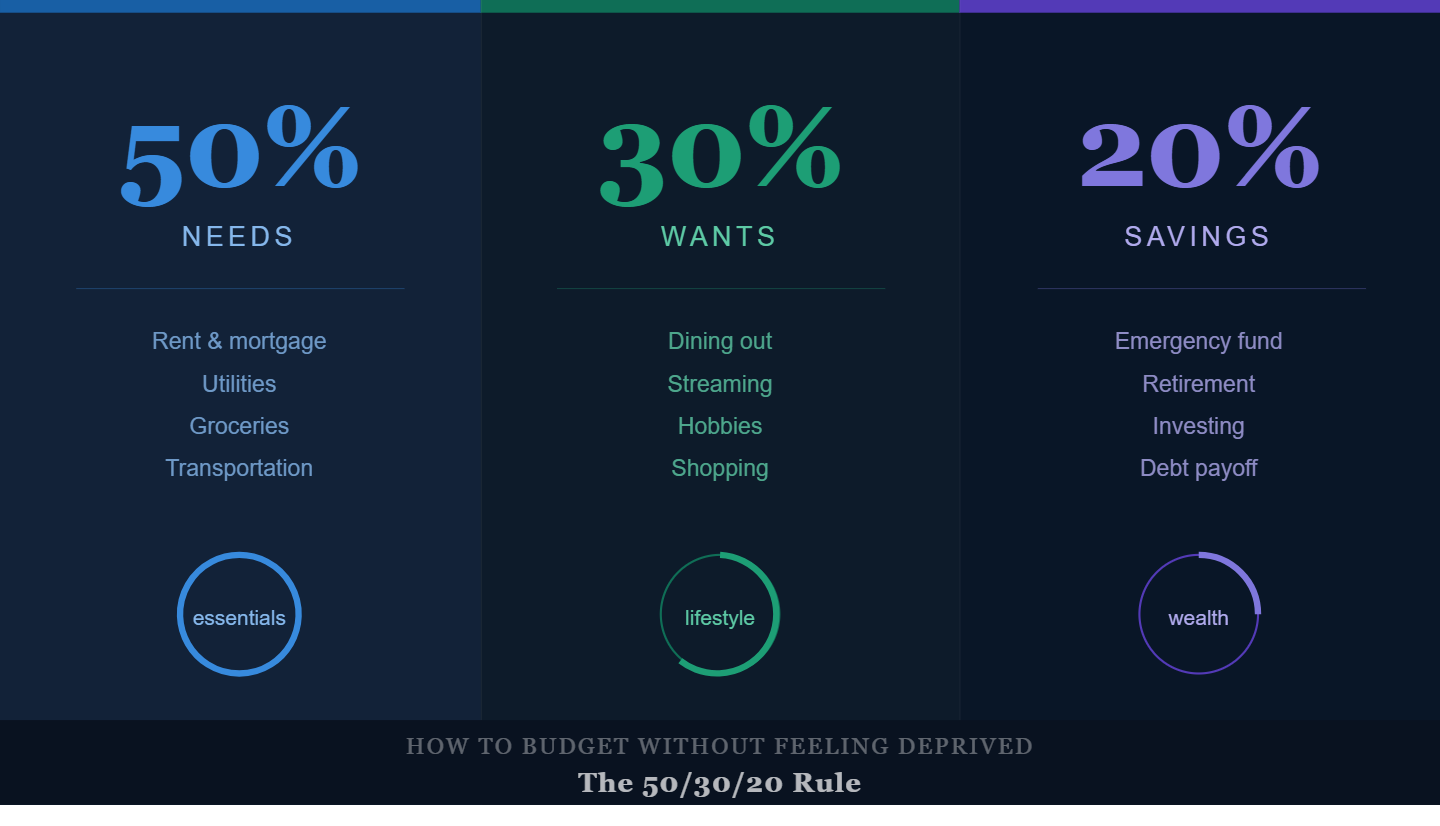

| The 50/30/20 rule splits your take-home pay into three buckets — so you can build wealth without giving up the life you actually enjoy. |

Most people approach budgeting like a crash diet. You restrict yourself so heavily for two weeks, you feel completely miserable — and then you “binge-spend” on a Saturday afternoon to compensate. The clothes pile up, the restaurant bills stack, and by Sunday night you’re back to square one, too guilty to even open your banking app.

Sound familiar? You’re not alone. Study after study shows that the majority of people who start a budget abandon it within the first month — not because they’re bad with money, but because the system they’re using punishes them for being human.

Here’s the good news: you don’t need a spreadsheet that tracks every single coffee purchase. You don’t need to give up your Friday night dinners or your streaming subscriptions. And you certainly don’t need a mathematics degree to figure this out. What you need is a simple, forgiving framework that works with your lifestyle instead of against it.

Enter the 50/30/20 Rule — arguably the most approachable and effective personal budgeting method ever created. Let’s break down exactly what it is, why it works, and how you can start using it today.

What is the 50/30/20 Rule?

The 50/30/20 rule is a straightforward method for dividing your after-tax income into three meaningful categories. The idea was popularised by US Senator and bankruptcy expert Elizabeth Warren in her book All Your Worth, and it has since become one of the most widely recommended starting points in personal finance — cited by financial advisors, robo-advisors, and money coaches alike.

The core concept is simple: once your paycheck hits your account (after taxes), you divide that money into three buckets — 50% for your needs, 30% for your wants, and 20% for savings and debt repayment. That’s it. No 47-line spreadsheet, no envelope system, no colour-coded categories for every latte and Uber ride.

The genius of the 50/30/20 rule is not that it’s the most optimised budget in the world. It’s that it’s optimised enough — and simple enough — that real people actually stick to it. It gives you clear guardrails without turning financial management into a part-time job. Think of it less as a budget and more as a compass: it keeps you pointed in the right direction, even when life gets complicated.

The Three Buckets Explained

Let’s get specific. Here is what each bucket actually means — and more importantly, what goes inside it.

Bucket #1 — 50% for Needs (The Essentials)

Half of your take-home income should cover the things you absolutely cannot live without. These are non-negotiable expenses — they would exist whether you liked them or not. If you lost your job tomorrow, these are the bills you’d still have to pay.

This includes:

- Rent or mortgage

- Utilities (electricity, water, internet)

- Groceries

- Minimum debt payments

- Transportation and insurance

- Essential medications

The tricky part here is honestly categorising what counts as a “need.” Your rent is a need. A Netflix subscription is not — even if it feels essential at 10pm on a Wednesday. If your needs category is pushing above 50%, that’s a signal worth paying attention to. It usually means one of two things: your fixed costs (especially housing) are too high relative to your income, or you’ve been unconsciously labelling wants as needs.

If you live in a high cost-of-living city and getting below that 50% threshold feels impossible, don’t panic. The 50/30/20 rule is a guideline, not a law. Some financial planners recommend a 60/20/20 split for people in expensive cities, and that’s a perfectly reasonable place to start.

Bucket #2 — 30% for Wants (The Secret to Sustainability)

This is the bucket that makes the 50/30/20 rule genuinely different from other budgeting systems — and the reason people actually stick with it.

Most budgets that fail do so because they treat every non-essential expense as a moral failing. Ordered a pizza? Guilty. Bought a book you didn’t strictly need? Irresponsible. Got a manicure? Shameful. That kind of thinking creates exactly the same cycle as crash dieting: restriction, deprivation, explosion.

The 30% wants bucket is the system’s official permission slip. It’s the acknowledgement that enjoying your life is not a financial crime. Your Saturday morning coffee? It belongs here. Your Spotify subscription, your gym membership, your occasional splurge on a nice dinner out — this is exactly where they should live.

This bucket covers things like:

- Dining out and takeout

- Streaming services (Netflix, Spotify, Disney+)

- Hobbies and gym memberships

- Non-essential shopping and clothes

- Travel and weekend experiences

- Personal care and beauty

The key distinction: a want is anything you’d choose to live without if you had to. The moment you genuinely could not function without something — emotionally, physically, professionally — it starts edging toward “needs” territory. But most things that feel essential really are wants, and that’s completely okay. Just put them in the right bucket.

A budget that makes you miserable is a budget you won’t follow. The 30% wants bucket isn’t a flaw in the system — it’s the whole point.

Bucket #3 — 20% for Savings and Debt Repayment (The Wealth Builder)

This is the bucket that separates people who build wealth from people who wonder where their money went. Twenty percent of your take-home pay, directed consistently toward your financial future, is genuinely life-changing — not in a motivational-poster way, but in a mathematical, compound-interest, retire-with-dignity way.

This bucket includes:

- Emergency fund (3–6 months of expenses)

- Retirement contributions (401k, IRA)

- Extra payments on high-interest debt (credit cards first)

- Investing in index funds or the stock market

- Saving for a house deposit

The order of priority within this bucket matters. Most financial experts suggest building a starter emergency fund (around $1,000) first, then aggressively paying down any high-interest debt, then building a full emergency fund, and finally focusing on long-term investing and retirement contributions.

One non-negotiable: if your employer offers a 401(k) match, always contribute enough to capture the full match before doing anything else with this 20%. That match is an instant 50–100% return on your money. Nothing in the market comes close to that.

To put the power of this bucket in perspective: on a $2,000 monthly take-home, 20% is $400 saved per month. That’s $4,800 in year one alone — without earning more, without a side hustle, just by directing money you already make into the right place. Invested at an average 7% annual return over 25 years, that becomes roughly $250,000. The math is not magic. It’s just consistency.

Why Most People Fail at This

The 50/30/20 rule is not complicated. The math is simple enough to do on a napkin. So why do so many people still struggle to make it work?

The answer is almost never the system — it’s the awareness. The single biggest reason people fail at budgeting isn’t that they don’t understand percentages. It’s that they have no clear, real-time picture of where their money is actually going.

Without tracking, that 30% wants budget quietly becomes 45%. The “quick” DoorDash orders, the impulse Amazon purchases, the round of drinks you didn’t plan for — individually, each one feels insignificant. Collectively, they devour your savings allocation before the month is even half over. And because there’s no visible scoreboard, you don’t realise what’s happened until you check your bank balance and feel that familiar sinking feeling.

The second most common failure mode is waiting for the perfect moment to start. People tell themselves they’ll begin budgeting after the holidays, or after the big work project, or once their income is a little higher. In reality, the best moment to start is always the one you’re currently in — imperfect circumstances and all.

The third issue is all-or-nothing thinking. People miss their targets for one week, decide the whole system is broken or that they’re too undisciplined to budget, and quit entirely. In reality, a budget you follow imperfectly 80% of the time will still transform your finances over a year. Progress beats perfection every single time.

How to Get Started Today

Here’s a practical, no-overwhelm approach to implementing the 50/30/20 rule starting right now — not next Monday, not next month.

Step 1: Calculate your actual take-home pay.

This is your income after taxes, not your gross salary. Check your most recent paycheck or bank deposit. If your income varies, use your average over the last three months.

Step 2: Pull up your last 30 days of bank and card statements.

Don’t judge what you find — just observe. Sort each transaction into one of the three buckets: need, want, or savings.

Step 3: Compare your actuals to the targets.

How close were you to 50/30/20? Most people are shocked to find their “wants” spending is well above 30%. That’s not a moral failure — it’s information.

Step 4: Automate your savings immediately.

The moment your paycheck arrives, set up an automatic transfer of 20% into a separate savings account. When the money is gone before you can spend it, the system works without relying on willpower.

Step 5: Check in weekly, not daily.

A brief 5-minute weekly review is enough to keep you on track. Daily obsessing leads to anxiety. Never checking leads to overspending. Weekly is the sweet spot.

Give yourself permission to not be perfect in month one. The goal for the first 30 days is simply awareness — knowing your numbers. Month two is for nudging those numbers toward the targets. By month three, the system starts to feel natural.

Final Thought: The Goal Is Freedom, Not Restriction

The entire point of budgeting is not to make your present life miserable so your future self can be comfortable. The point is to build a life you can enjoy now and sustain for decades. The 50/30/20 rule is one of the most effective tools for doing exactly that, because it starts from a position of generosity rather than deprivation.

You are allowed to spend money on things that bring you joy. You are allowed to eat at restaurants, travel, buy clothes, and invest in experiences that matter to you. The 30% wants bucket is not a bug — it’s a feature. It’s what makes this approach human, sustainable, and worth doing.

The only thing standing between where you are now and genuine financial confidence is a clear view of your numbers and a simple system to guide your decisions. You now have the system. All that’s left is the first step.

You don’t have a budgeting problem.

You have a tracking problem.The 50/30/20 rule only works when you know exactly where your money is going.

That’s what my Money Mastery System is built for.

If you’re serious about fixing your finances:

Stop reading. Start executing.